With the advent of digital banking, more and more people are banking remotely via their personal computers and mobile devices. But while digital banking options have been on the rise for years, physical bank and credit union branches are still important to consumers.

Even so, branches will need to transform to remain relevant. “Just under two-thirds of banking executives agreed that the [traditional] branch-based model will be ‘dead’ within five years,” The Financial Brand reports; branch transformation will be essential in today’s digital-centric environment.

Indeed, retail banking must span both digital and physical environments—with unique value in each complementing the other. In this article, we explore how the COVID-19 pandemic has affected consumer banking behavior; how retail banking will span these environments; and how these elements will shape future branch strategies.

Recent Consumer Trends in Retail Banking

Before the pandemic, consumers were already increasing their use of digital banking tools. They were also banking remotely in increasing numbers, whether that meant banking via an app on their mobile device or banking over the internet with a desktop computer or laptop.

Convenience, access to products and services, and security were top priorities among consumers in both physical and digital environments. Even then, banks could increasingly meet these needs in standalone digital environments with multi-factor identification, banking apps, and chatbots, among other tools.

Given the limitations imposed by the COVID-19 pandemic from 2019 to today, consumer habits have shifted even more dramatically towards digital. Beyond checking balances and transferring money between accounts, consumers have begun using their devices to remotely open new accounts, apply for loans, and engage in other ‘high-touch’ activities traditionally carried out in physical branches.

Adapting Branches Models for a New Multi-Channel Approach

Physical bank branches have seen a decrease in traffic as the COVID-19 pandemic has grown and as remote digital capabilities have become more sophisticated. Now, “85% of Americans say they will use digital tools to complete some or all financial transactions after the pandemic,” Forbes reports.

Banks have been closing some physical bank branches as a result; in many cases, they are reapplying those investments to digital channels, supporting even more complex interactions and transactions without requiring customers to set foot inside a physical location.

But while a branch-centric model may no longer be relevant, branches remain ideal environments for face-to-face consultations and many high-value transactions. A branch resurgence would mean new opportunities for banks as the roles of their branches evolve—assuming banks can meet consumers’

expectations for personalization, security, and convenience.

Four Opportunities to Improve In-Person Retail Banking

Consumers will continue to prioritize physical branches for certain banking needs. Some banks may require certain functions involve a physical visit to bank branches as well. This means that banks should invest in both their digital and physical banking environments.

But banks and credit unions must determine how the two environments will complement one another to provide consumers with a better, more holistic banking experience. Here is a closer look at some methods banks can adopt to improve customer experiences, customer outcomes, and business results.

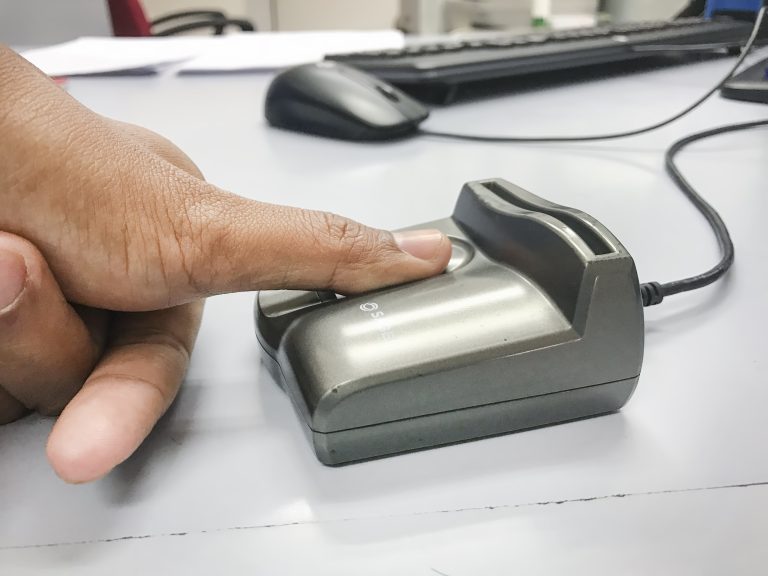

1. Advanced Security Across Environments

“Over 96% of consumers want security and fraud protection features from their banks,” The Motley Fool reports—whether that applies to physical or digital environments. But as consumers increase their use of digital security features, they will expect a more seamless yet robust security infrastructure across physical and digital environments as well.

Banks should continue to create mobile banking apps that are easy to use and have enhanced security features. Those security features should align seamlessly with physical branches as well—for example, biometric data for consumers who prefer to use their fingerprints in both branches and on their personal devices; or, multi-factor authentication that can be used in both environments; among others.

2. Appointment Scheduling

Suffice it to say, consumers simply won’t tolerate waiting in line at a bank branch anymore. Banks can adopt appointment scheduling software, enabling customers to schedule appointments for in-branch banking services from their personal devices for the times that work best for them.

Investment in these technologies is growing, where 35% of banks already used appointment scheduling in 2020. This makes banking more efficient and aligns the convenience of digital environments with physical branch experiences.

3. In-Branch Devices for Customers and Employees

Modern consumers expect to expedite in-branch experiences with the use of digital tools. These expectations are shaped by other consumer experiences, such as digital kiosks in airports and in retail stores. These devices can be used to access critical customer data, scan documents, or execute online transactions in real-time during customer visits.

“The same technology that powers digital banking can also be used to enhance the branch experience,” BizTech describes. “Whether it’s for customers waiting to be helped, bank employees trying to help the most people, or keeping the line moving swiftly, banks are harnessing mobility to improve the in-branch experience.”

4. More Personalized Services

Advanced digitization, authentication, and access to customer data can help branch employees better personalize experiences for their customers. This is critical as consumers increasingly use remote digital tools for basic transactions and prioritize branches for complex or interpersonal interactions.

Banks should prioritize going beyond customer expectations during branch visits as well. “This, in our view, is the true promise of personalization in retail banking: being able to go beyond next-best offers and targeted marketing and create more customized, relevant end-to-end experiences for customers,” Boston Consulting Group (BCG) describes.

For example, branch staff can take on a more personal consultative role, accessing analytics based on an individual customer’s financial opportunities and habits. A branch employee might make recommendations about how that customer can pay off a mortgage more quickly, consolidate debt, or make smarter investments, among other possibilities.

When There is No Substitute

For banks unsure about how to pursue a new in-branch strategy, they can begin by identifying the customer interactions for which there is no real digital substitute available to them. Banks that cannot successfully implement remote video chat, for example, can’t necessarily expect to substitute complex interpersonal interactions with a digital-only exchange. Instead, they can focus on enhancing their in- branch experiences to make them more appealing for modern consumers.

The most successful banks in the future will be those who use their physical branches to provide exceptional customer experiences based on modern consumer expectations. They will invest in digital banking tools so that they can serve customers no matter what banking method they prefer. Most of all,

banks and credit unions of all sizes should lean into what they do best—whether it’s serving a local community or providing advanced investments services—and secure the right strategies and technologies that contribute to those ends.

Partner with Semifly as You Develop Your New Branch Strategy

The consultants at Semifly can help as you prepare your own next-generation branch strategy. Contact one of our finance industry experts and begin a conversation about your future branches today.

Unregistered User

It seems you are not registered on this platform. Sign up in order to submit a comment.

Sign up now